Abstract

- Good companies with managements that are able to allocate capital efficiently in one of 6 ways (cf. below) have the potential to be lucrative longterm investments.

- A “good business” is a franchise that is protected by a moat based on 1) intangible assets, 2) high switching costs, 3) network effect, or 4) low-cost production.

- A Discounted Cash Flow (DCF) analysis seeks to appraise the here-and-now value of the business based on expectations of future free cashflow or earnings. The following variables go into a valuation based on the DCF methodology: 1) earnings power (EPS), 2) growth rates, 3) dividend payout ratio, 4) future P/E multiple, and 5) discount rate(s).

- DCF analyses are packed with subjectivity and assumptions, which is why venturing into such is an ungrateful job. According to legendary value investor Seth Klarman, it is, however, the investor’s best valuation tool.

Why are we so clueless about the stock market? is a fairly easy and short book, but boy, it’s filled with a bunch of concrete and applicable advice, formulas and models.

What makes investors rich?

The author, Mariusz Skoniecznys, argues that fantastic businesses with competent management teams that are able to efficiently allocate capital are able to grow investors’ wealth. He presents six ways in which a company can allocate capital and thus increase the value of the company on behalf of its owners (the shareholders). The business can 1) reinvest in the business’ productive infrastructure (maintaining production levels); 2) return the profits to shareholders via dividends; 3) share buyback programmes; 4) reducing debt and hence the interest expenses, which lessens the vulnerability when facing headwind; 5) reinvest in the company’s growth by allocating capital to R&D efforts, production facilities, equipment and hiring employees; 6) acquisitions of other businesses.

In short, good businesses with competent capital allocators in the management team are likely to be lucrative investments.

What is a good business?

In length of the previous section, Mariusz explains that good businesses are those that can consistently achieve a high return on capital. These businesses often posses a competitive advantage, or moat in Warren Buffett’s terminology. Mariusz takes a point of departure in Pat Dorsey’s The Little Book that Builds Wealth to outline the four types of moats that allow a business to earn an above average rate of return on capital:

- Intangible assets such as brand value, patents and licenses. A strong brand enables the company to e.g. charge a higher price than the competitors. It further ensures the company’s pricing power, hence allowing it to raise prices alongside inflation. Patents hinders competitors to copy one’s products. Licenses are difficult to obtain, so once you possess one/more, it’s a lucrative advantage that one can capitalize on while the competitors play catch-up.

- If the switching costs are high, it’s less likely that one’s customers will leave you for the benefit of the competitors. For instance, two B2B enterprises may be intertwined after years of collaborating, and switching vendor would require investments in IT systems, education, training etc.

- When the number of customers/users of one’s service, e.g. a dating site, increases, so does the value of the business due to the network effect. Everyone has a Facebook-profile because everyone has a Facebook-profile, right?

- Businesses that are able to achieve higher margins than the industry average possess a cost advantage, since they can undercut rivals’ prices and garner more capital to allocate in one of the aforementioned 6 ways.

Mariusz argues that businesses whose profitability beats the industry average and have competent capital allocators in the management team possess an edge, which will most likely be reflected in the stock’s price over time.

(Discounted) Cash is King

Chapter 5 of Mariusz’ book is probably the best exposition of the Discounted Cash Flow (DCF) method I’ve read. The method struck me as rather complex the first time I delved into it. Mariusz made it quite clear, though, so I hope I’m able to do his explanation justice below.

By applying the DCF method, an analyst attempts to assess what a business’ here-and-now value is based on the future free cash-flow or earnings that business will generate. First, the analyst should arrive at a conservative assumption of how much capital the business is able to distribute via dividends and/or add to the stockholders’ equity based on 1) a ‘normalized’ cash-flow or earnings in year one, and 2) a growth rate, which that cash-flow or earnings will compound at. For instance, let’s assume we have a business that earns $10 after having adjusted for one-time events and/or cyclicality (hence normalized, though it’s quite simplistically put), and we assume said earnings grow by 5% a year over the next 5 years, the business’ future earnings are offhand worth $12.76 (10*1.05*1.05*1.05*1.05*1.05 = 12.76).

However, we haven’t yet considered the discounting aspect. There is a cost associated with tying up capital in anything. First, we got the ever-present tax on capital: inflation. If we assumed that you get 0.5% on a bank account, and inflation is 2%, you lose 1.5% of buying power each day your capital is tied up in the bank account rather than something that yields more than 2%. This something could be a longterm Danish or US government-issued bond that essentially yields a risk-free 3% interest. By choosing to own the aforementioned business that (simplistically put) yields a 5% return, you simultaneously deselect the government bond because you’re willing to assume more risk with the prospect of getting a 2% higher return. This ‘extra’ above the risk-free rate is your risk premium.

You decide, however, that a 2% return above the risk-free rate is not sufficient for the extra risk you take on. You know that that stock markets have historically returned 7-9% annually on average over the last century. Hence, you determine that 7.5% is your minimum return requirement. This required rate of return is your discount rate. This percentage is thus what you should be discounting the cash-flows or earnings with. Hence, the current value of the future earnings is $8.9 (12.76/1.075/1.075/1.075/1.075/1.075 = 8.9).

How does one settle on a discount rate? Mariusz recommends that you have at it logically. Let’s say the passive bank account yields 0.5%, so it must be higher than that. A practically risk-free government bond yields 2.5%, so we must beat that as well. Highly ranked corporate bonds yield 4-6% (remember, this is purely hypothetical), so we must amp up further. In other words, we have to arrive at a discount rate that is well-above the risk-free or ‘safe’ rates. Mariusz mentions that a rate somewhere between 7-13% is usually the sweet spot. The lower end can be applied for stable stocks such as Coca-Cola, Gillette and P&G that are not affected particularly much by e.g. cyclicality. The two-digit discount rates should be applied to more uncertain investments where we can’t predict the future as easily as with the more ‘bond-like’ stocks. In essence, you should adopt a higher discount rate for the more uncertain investments as a compensation for the (perceived) extra risk.

Allright, so once you’ve settled on a discount rate, you need to make some additional assumptions: What do you expect the earnings will grow at for the time horizon your analysis is covering? Furthermore, what P/E multiple do you assume the stock will be traded at by the terminal year (e.g. year 5)? The latter assumption has a huge influence on the calculated intrinsic value, since it determines the trading price you expect to unload the stock at, since EPS in terminal year x P/E multiple = stock price in terminal year.

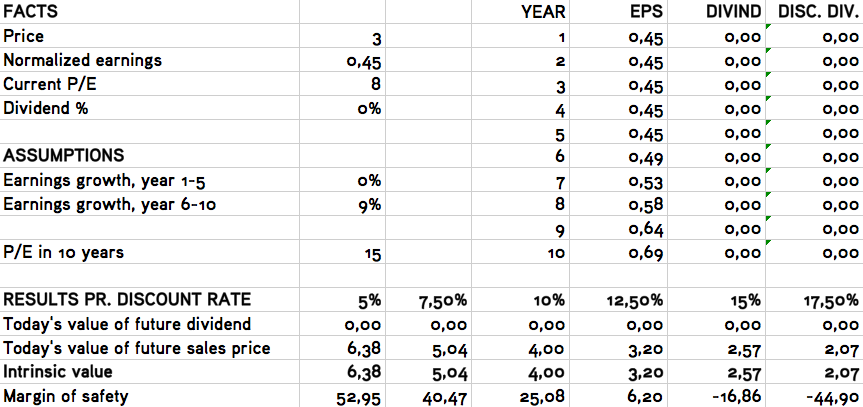

I know, I know. This walk-through is just a pile of numbers and long words. I hope, however, that the below DCF analysis (or DEF, discounted earnings flow) taken from my review of Sports Direct (SPD) may shed some light on the mystery.

I decided to acquire stocks in Sports Direct based on this analysis, since the intrinsic value of the business with a 7.5% discount rate is £5.04 relative to the then current trading price of £3. Even if I applied a 10% discount rate, I would achieve a 25% margin of safety, since £4 was the intrinsic value I arrived at.

It’s probably quite clear that a DCF analysis is packed with subjectivity and assumptions. I do not by no means claim that this method is the perfect way to value a business. Yet, according to legendary investor Seth Klarman, it’s the best tool in the investor’s tool box. If it’s still not entirely clear, I hope you’ll stop by my analyses of Sports Direct (SPD), Halfords Group PLC (HFD) and Domino’s Pizza Group (DOM), as you’ll get the context behind the growth and discount rates.

The pursuit of gold

Mariusz suggests you should start your pursuit for investment ideas by screening for businesses with a ROE above 15% and a stable earnings record. Next, look at the stock’s P/E and its 52-week price range. This should give the analyst an idea of the business’ current price level – expensive, moderate or cheap? Then, study the business, the industry, the competitors, the risks etc. Mariusz finally presents a list of questions you should seek to answer, e.g. about the business’ moat and whether it’s sustainable. In addition, ask yourself: Is the industry stable or subject to sudden transformation? Is the business simple and understandable? Most importantly, is the stock trading at an attractive price? Based hereon, determine whether the stock is a buy or a pass.

4 thoughts on “Book Summary of Why Are We So Clueless About the Stock Market?”