Reading Time: ~11 min.

Abstract

- RCI Hospitality Holdings Inc. (RICK) owns 45 strip clubs and 6 Bombshells (a franchise concept ala Hooters). Management implemented a disciplined capital allocation strategy in 2016 that primarily focuses on acquisitions of strib clubs at prices, which ensure a double digit annual return in free cash flow. Management has excelled in doing so, causing a 200% stock price appreciation during the past two years. The natural question is now: Are we late to the party?

- A discounted cash flow (DCF) analysis using a 9-10% discount rate suggests that a 30-60% upside potential remains as so forth the business can achieve an annual growth rate in free cash flows of 12.5% during the next six years.

- It’s an optimistic prognosis, but the business’ historic growth mixed with an ocean of potential acquisitions candidates in a market marked by few competing acquirers lie behind these rosy prospects.

- Other pluses include a high degree of insider ownership, high barriers to entry, and at least three catalysts that might drive afore intrinsic value estimate further north.

The ancient marketing slogan “sex sells” is certainly substantiated when one looks at the books of the american market leader of strip clubs, RCI Hospitality Holdings Inc. (RICK).

The Business

RCI is a holding company that owns an array of businesses within the entertainment and restaurant industry divided into two areas:

Nightclubs (adult entertainment) counts strip club franchises such as Rick’s Cabaret, Jaguar’s Club, Tootsie’s, Club Onyx and 11 other brands. Bombshells is a franchise like Hooters, i.e. restaurants plastered with flat screens and daringly dressed waitresses. According to the latest Q10, the revenue is split 85-15 between Nightclubs and Bombshells, respectively.

The Stock

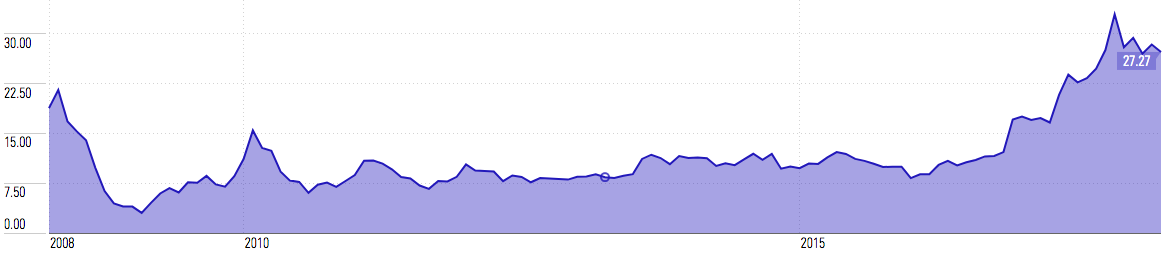

The stock reflects that RCI has experienced a few profitable seasons, especially since 2016 when management implemented a disciplined capital allocation strategy in 2016 that primarily focuses on acquisitions of strip clubs at prices, which ensure a double digit annual return in free cash flow. Management has excelled in doing so, causing a 200% stock price appreciation during the past two years, from $9 to $27, cf. below chart.

The current price of $27 translates into a P/E of 13, P/BV of 1.8 and P/S of 1.75. These ratios don’t scream “bargain”, but nor does it sound exorbitant for a business that has increased its operating income with 12% annually during the past five years.

The natural question is now: Have we arrived too late to the party? Let’s try to estimate RCI’s intrinsic value to answer that question.

Valuation

A discounted cash flow (DCF) analysis seems to be the most appropriate method to value RCI, since 1) growth in FCF is the company’s measurement for ‘success’ as well as the crux of management’s capital allocation strategy; 2) FCF growth is the metric used by management to conjuncture about future performance; 3) and RCI has displayed a stable historic development in FCF growth, which has been in line with management’s past announcements.

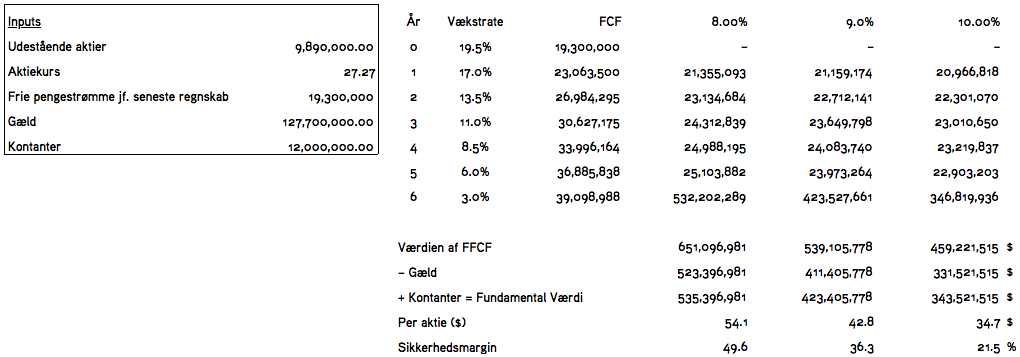

The DCF method is outlined in the post How much is LEGO worth?, but let me flesh it out quickly. You may have heard Warren Buffet say: “Intrinsic value can be defined simply: It is the discounted value of the cash that can be taken out of a business during its remaining life.” A DCF calculation aims to determine just that. The model seeks to estimate a company’s present value based on the future free cash flows of the business (into perpetuity). In essence, free cash flow (FCF) is the profits that are left after spending the money needed to maintain the operational assets (e.g. property, plant and equipment). Hence, the free cash flow is simply operating cash flow – capital expenditures. FCF is significant, as it represents 1) the cash you could pocket if you owned the entire business, and/or 2) the cash the company can allocate as it sees fit, e.g. reinvest in the business’ growth, pay dividends or share buyback programs. Once we’ve made our projections as to the growth rate of these free cash flows, we need to settle on an appropriate discount rate based on the investment’s risks. Finally, we subtract the business’ long-term liabilities ($127.7 million in RCI’s case) and add its cash position ($12 million).

Let me briefly voice the considerations that went into my growth and discount rate estimates.

Our starting point – the latest announced free cash flow number – is $19.3 million. Management recently said its ambition of hitting $23 million in FCF was on track, a growth rate of 19.5%. Given the management’s ethos, I dare to trust this number. The subsequent five years are more ‘fluffy’ and subject to guesswork. Management says it expects FCF to grow at 10-15% annually. We can plot these ambitions into the model in numerous ways, but let’s assume a gradual decline from 19.5% to the annuity growth rate of 3% in year 6; this corresponds to an average growth rate of 12.5% in the period. These assumptions produce an intrinsic value span of ~$35-$54 depending on the discount rate (cf. below).

To arrive at a discount rate, let’s try to calculate RCI’s weighted average cost of capital (WACC). The term is outlined in more detail in How much is LEGO worth? and Find the Best Stocks, so I’ll just present the numbers here. RCI’s capital structure is made up of 54.4% in debt and 45.6% equity. The average interest on the debt is 6.73% cf. page 8 of the latest Q10. If you demand a 14% return on your investment (which is the current ROE of RCI), you would end up with a discount rate of 10%, cf. below calculations:

- Cost of debt: 6.73% x 54.4% = 3.66%

- Cost of equity: 14% x 45.6% = 6.38%

- Cost of capital: 6.38 + 3.66 = 10.04%

As I would ‘demand’ a 12-14% return on my investment, my estimate of RCI’s intrinsic value is $35-$43 per share, an upside potential of 30-60% from the current price of $27.

Capital Allocation

Since the CEO, Eric Langan, implemented a disciplined capital allocation strategy in 2016 RCI has employed capital only when 1) the investment in new or existing clubs can produce a 30% return; 2) under-performing clubs/investments must be sold to free capital that can be employed more effectively elsewhere; 3) share buyback programs are launched when RCI trades at a P/CF of 10 or below; 4) the most expensive debt is paid down quickly as so forth it makes sense from a tax perspective.

Management has “walked the talk”, i.e. by buying back 7% of the outstanding shares in 2016 when RCI traded at around $10. Furthermore, RCI acquired Scarlett’s Cabaratt, which generated $13 million in revenues and $6 million in EBITDA, for $26 million. On several occasions has RCI acquired businesses at only 3-4 EBITDA.

Moat

There are about 4,000 strip clubs in the US and very rarely are new licenses issued. The industry hence benefits form high barriers to entry. Furthermore, the market is fragmented and most clubs seem to be owned by private individuals, which is one of the reasons why RCI has been able to make aforementioned ‘bargain’ acquisitions. In my humble opinion, RCI’s moat is rooted in its ability to acquire businesses at bargain prices in a sinful industry where there are few competing acquirers.

Risks

RCI presents an array of risks on page 8-15 of the annual report. However, I feel the need to stress that the industry is “extremely volatile” according to management. If a community or country’s economy goes through a rough patch, a visit to the local strip club is one of those ‘expenses’ that are stripped easily. Advocates of legal action towards strippers’ terms of employment, serving of alcohol, expiration of licenses are of course too dangers of a sinful industry.