A wise man once told me: “Never recommend a stock to anyone. You’re bound to loose. If it rises, they’re brilliant. If it tumbles, you’re an idiot.” In length, I emphasize that the following write-up is not a recommendation. It’s merely a collection of reflections that document my reasoning behind my investment decisions, hence allowing me to go back and learn from my mistakes and successes.

Abstract

- Stocks within the non-cyclical consumer goods sector have earned their nickname “expensive defensives” due to their high P/E, P/BV and P/S multiples. Investors must feel that the perceived safety in consumables is worth coughing up for.

- Even after a 30% slash in Reckitt Beckisers’ stock price, it still appears considerably overvalued. If consumables can tumble that much and still not be a bargain, can one hope to find a bargain in this sphere?

- A ‘study’, which mechanically calculates intrinsic values for 25 consumables stocks with P/E multiples below 25, seeks to determine just that. It concludes that among these select 25 stocks, most are indeed overvalued. However, one stock appears outright attractive, and two others deserve a closer look.

I’ve been eyeballing various stocks within the realm of consumables for a while. As you may know, I consider the markets to be quite ‘expensive’ (read Why I’m hoarding cash and praying for the crash), and consumables may not be the worst businesses to own in case of a recession. People can’t function without groceries and healthcare products, so why not own stocks of the suppliers of said products?

Price has kept me on the sidelines. For instance, Walmart, Nestle, Colgate-Palmolive and Costco are all part of the category “expensive defensives” given their P/E multiples around or above 30. Furthermore, Reckitt Benckiser, a British consumables supplier, has tumbled 30% since medio 2017, and is still more expensive than it is defensive (a discounted cash flow calculation using a 3% growth-rate and 10% discount rate returns an intrinsic value estimate of ~£30; it’s currently trading at £57).

Yet, I figured there must be value somewhere in the non-cyclical consumer goods sector, so I decided to conduct a ‘study’ to check it out.

Outlining the Study

I don’t have a Bloomberg terminal or other tools reserved for finance professionals, so I couldn’t set-up a full-blown automatic screening process that outputted all stocks from this and this sector that match these and these criteria and are undervalued given such and such growth and discount rates.

I instead took a point of departure in my watchlist, which I’ve built up over time. This list contains various stocks I would like to own – at the right price. I narrowed-down the list so that it only contained so-called defensive, mostly non-cyclical stocks, which traded below a P/E of 25. I then excluded companies with a history of negative or irregular free cash flows (i.e. GlaxoSmithKline PLC and The Kraft Heinz Co).

Based on this gross list, I wanted to get a quick overview of which stocks might be undervalued. Hence, I automated the intrinsic value calculation process based on a set of simple criteria. Following that exercise I had a list of six candidates, which I wanted to check out. I thus dive into each one’s historic performance to assess which appeared most undervalued, so I could determine which might be worthwhile to analyze further.

Conducting the Study

As mentioned, the first step was to compose a list of consumables stocks with a P/E of below 25 from my watchlist (P/E multiples in parentheses):

| CVS Health Corp (10.7) | Big Lots, Inc. (12.36) |

| Dollar Tree, Inc. (12.87) | Target Corporation (15.06) |

| Tyson Foods, Inc. (15.32) | Imperial Brands PLC (17.6) |

| Molson Coors Brewing (17.94) | Kimberly Clark Corp (18.09) |

| Henkel AG (18.10) | Altria Group, Inc. (18.43) |

| British American Tobacco PLC (18.76) | General Mills, Inc. (18.84) |

| Dollar General Corp. (19.26) | Kellogg Company (19.32) |

| Walgreens Boots Alliance Inc. (19.5) | Smith & Nephew PLC (20.13) |

| Procter & Gamble Co (20.41) | Lowe’s Companies, Inc. (21.21) |

| Diageo PLC (21.66) | Philip Morris International, Inc. (22.08) |

| PepsiCo, Inc. (22.09) | Unilever PLC (22.49) |

| Danone SA (23.02) | Clorox Co (24.13) |

| Johnson & Johnson (24.65) |

Multiples as of March 9, 2018

The next step was to quickly assess each stock’s intrinsic value. The most widely used approach to assessing such values goes under the banner discounted cash flow (DCF) analysis. The method is outlined in the post How much is LEGO worth?, but let me flesh it out quickly.

You may have heard Warren Buffet say: “Intrinsic value can be defined simply: It is the discounted value of the cash that can be taken out of a business during its remaining life.” A DCF calculation aims to determine just that. The model seeks to estimate a company’s present value based on the future free cash flows of the business (into perpetuity). In essence, free cash flow (FCF) is the profits that are left after spending the money needed to maintain the operational assets (e.g. property, plant and equipment). Hence, the free cash flow is simply operating cash flow – capital expenditures. FCF is significant, as it represents 1) the cash you could pocket if you owned the entire business, and/or 2) the cash the company can allocate as it sees fit, e.g. reinvest in the business’ growth, pay dividends or share buyback programs. Once we’ve made our projections as to the growth rate of these free cash flows, we need to settle on an appropriate discount rate based on the investment’s risks. Finally, we subtract the business’ long-term liabilities and add its cash position.

I did the above for all 25 stocks. For each, I found the latest FCF number as well as the company’s debt and cash positions. As mentioned, I needed to automate the process, since I couldn’t assess the appropriate growth and discount rates for each company. I decided to use a 3% growth rate from year 1 into perpetuity across the board, as this has been the growth rate for the overall economy historically. I found it to be quite the diplomatic solution. Then, I figured a discount rate between 7.5% and 10% was appropriate for these “defensive stocks”. The below stocks turned out to be undervalued based on this mechanic process:

| Stock | Price | IV, 7.5% | IV, 10% |

| Unilever PLC | £38.94 | £79.13 | £45.86 |

| Big Lots, Inc. | $48.45 | $115.50 | $72.32 |

| Henkel AG | €104.00 | €144.19 | €88.56 |

| Imperial Brands PLC | £25.92 | £53.00 | £28.87 |

| Target Corporation | $70.49 | $143.5 | $84.9 |

| Walgreens Boots Alliance Inc. | $70.60 | $119.46 | $70.78 |

Stock prices as of March 9, 2018

Though this process of applying a ‘mere’ 3% growth rate might have excluded some of the original 25 stocks from entering the undervalued shortlist, let’s assume that the above six stocks constitute the seemingly not-so-expensive defensives.

I went on to assess whether each stock’s intrinsic value estimate were based upon too conservative or too generous growth rates. I thus took a quick look at the six candidates’ past performance in order to assess each business’ normalized free cash flow growth.

| Stock | 1-year % | * 5-year % | * 9-year % |

| Unilever PLC | 12.3% | 5.7% | 2.8% |

| Big Lots, Inc. | -16.7% | 4.3% | 5.7% |

| Henkel AG | -22.9% | 0.1% | 11.4% |

| Imperial Brands PLC | -3.9% | 6.6% | 0.26% |

| Target Corporation | 19.1% | 17.7% | 20.2% |

| Walgreens Boots Alliance Inc. | 7.4% | 15.5% | 12.5% |

* Percentages are on a compounded basis.

Looking at the above tables, I’d say Unilever, Walgreens and Target deserve a deeper look. Especially the latter looks interesting given its consistently high free cash flow growth.

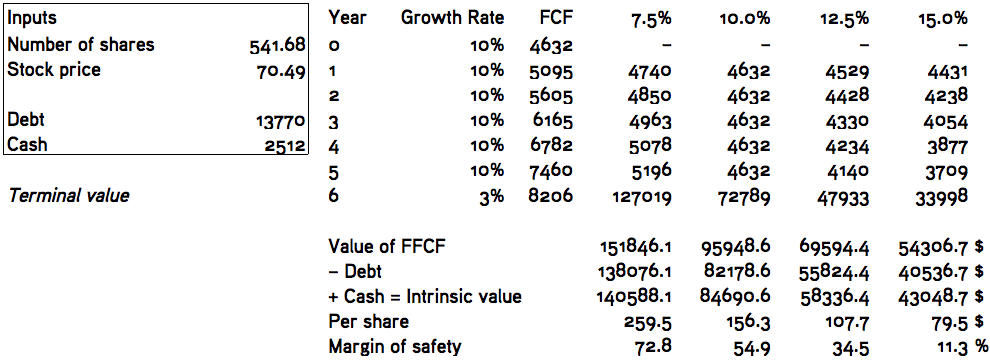

Unless some factors in the industry threaten Target’s ability to continue this trend (I haven’t analyzed it, yet), I’d say its historic performance merits a growth rate above 3%. If one dares to apply, say, a 10% growth rate to Target’s FCF five years out followed by a perpetuity growth rate of 3%, one would get an intrinsic value estimate of $156.3, cf. below calculations – an upside of 122%! Surely, this is too optimistic or something is ‘hidden’ behind these numbers, as a big-time player such as Target can’t be this undervalued. Yet, my curiosity is intrigued.

Conclusion

Based on this (very) small, hand-picked segment of global consumables stocks, I’d say the nickname “expensive defensives” is well-deserved. Only one looks outright attractive (Target) while Unilever and Walgreens’ price look fairly attractive. Big Lots might appear cheap, but it’s 1-year FCF development indicates some headwind. Henkel’s and Imperial Brand’s FCF history is not stunning, so I’m offhand not inclined to dive further into these.

The outcome of this study is thus a shortlist of stocks I will now double-click on – starting with Target. If I don’t find anything grave when digging deeper into Target, this might be the next addition to my portfolio. One stock analysis coming up!

The Study’s Limitations

A few disclaimers and words of warning to end this blog post on. I didn’t look ‘behind’ the figures; maybe some non-recurring items ‘distort’ the numbers. I simply took the free cash flow, cash and debt positions at face value. The study was mechanic and selective. A far more interesting study would be a deep-dive into the entire universe of non-cyclicals and consumables where an automated system would apply appropriate growth rates based on historic performance. Now, that would be a research paper worth reading. I will, however, reserve that task for more resourceful parties – any takers?

One thought on “Are there any bargains among the “expensive defensives”?”